China’s Semiconductor Industry Avoids “Blockade Against Miniaturization”

“Chinese manufacturers are unable to import cutting-edge semiconductor manufacturing equipment such as EUV equipment. As a result, a large amount of direct government funding has flowed into manufacturing equipment for mature processes, leading to a massive increase in production.” In December 2024, CCTV published an article with the headline, “While the United States is tightening its chip sanctions, China’s semiconductor exports have surpassed one trillion yuan.”

Photo: Anatoly Morozov / PIXTA

The semiconductor friction between the United States and China is entering its eighth year. The US government sanctions since the first Trump administration have succeeded in blocking China’s development and production of advanced ICs. However, China is becoming more competitive.

Three Phases of US sanctions against China

The friction between the United States and China over semiconductors, a strategic material, entered its eighth year in the spring of 2025. The sanctions against China imposed by the first Trump administration were strengthened by the Biden administration and are now back in the hands of President Trump. The series of sanctions imposed by the US government can be summarized as a “blockade against miniaturization” of integrated circuits (ICs), but China’s semiconductor industry is gaining the competitiveness to evade them. Before looking ahead to semiconductor friction in the “another Trump” era, let’s look back at how the US and China came to be at odds over this issue.

In June 2014, China’s Xi Jinping leadership announced a new semiconductor support policy, the Guidelines to Promote the Development of the National Integrated Circuit Industry, “with the goal of establishing a world-leading semiconductor industry in all areas of the integrated circuit supply chain” by 2030. These guidelines differ significantly from previous semiconductor promotion policies in two ways. The first is that they emphasize national security, such as the need to domestically produce IC chips for communications. This was against the backdrop of the Xi leadership’s announcement in April of that year of a “holistic view of national security” that prioritized the stability and preservation of the Communist Party regime.

The second is that they clearly stated the establishment of a national fund for semiconductors, the China Integrated Circuit Industry Investment Fund (ICF), and actually launched the first phase (140 billion yuan [about 19.14 billion dollars]). Previous stimulus measures have focused on tax incentives, but a system has been established where the government “directly injects funds” to provide support.

In May 2015, the Chinese government announced its “Made in China 2025” industrial promotion policy, which aims to make China a “manufacturing powerhouse.” It placed semiconductors and other next-generation information and communications technology (ICT) at the top of 10 priority areas, and set a goal of increasing China’s self-sufficiency in ICs, which was 33% in 2016, to 58% in 2020 and 80% in 2030 (revised in 2017).

This clearly shows the security idea of eliminating foreign influence as much as possible in the procurement of semiconductors, which determine the performance of ICT equipment and weapons. In addition, the government also included the establishment of a second phase of the ICF (on the scale of 200 billion yuan).

At this time, China was on the verge of taking the lead in security-related ICT, such as artificial intelligence (AI) and the “5G” high-speed communications standard. The first Trump administration was wary of this trend spreading to semiconductors and moved to impose sanctions on China, criticizing “Made in China 2025” as a hotbed of unfair subsidies.

The series of US sanctions can be divided into three phases.

The first phase began in April 2018, when a seven-year ban was imposed on US companies doing business with Zhongxing Telecommunication Equipment (ZTE), a major telecommunications equipment manufacturer, for illegal exports to North Korea and other countries. ZTE, which used US-made ICs in its flagship smartphone products, fell into a management crisis and “surrendered” in July that year, agreeing to pay fines.

In October of the same year, the United States restricted the export of US-made manufacturing equipment to Fujian Jinhua Integrated Circuit Company (JHICC), which was seeking to enter the “DRAM” semiconductor memory market, citing a security risk and forcing the company to suspend its plans. In this phase, the US was unilaterally forcing weaker Chinese manufacturers to surrender.

In the second phase, the target was Huawei Technologies (Huawei), a symbol of Chinese high technology with its 5G-compatible smartphones and base stations. In December 2018, Canadian authorities, at the request of the United States, arrested the eldest daughter of the company’s founder, an executive, on charges of illegal exports to Iran, which were widely reported.

In May 2019, the Trump administration added the company to the “Entity List” (EL) under the Export Administration Regulations (EAR), which imposes export restrictions. Unlike ZTE, however, the company did not throw in the towel. It continued to design ICs at a subsidiary and continued to source communications ICs by outsourcing production to Taiwan Semiconductor Manufacturing Company (TSMC).

In response, the Trump administration tightened regulations in May 2020 to the point where the two companies could no longer continue to do business. TSMC complied with the administration’s wishes and stopped accepting new orders from Huawei.

In general, the finer the circuitry of an IC, the faster the computational speed and the lower the power consumption. And of course, the smaller the circuit, the smaller the chip will be. These are essential characteristics for logic (computing) ICs, which are the brains of smartphones. As of 2020, TSMC’s 5nm process (manufacturing technology) logic ICs were the most advanced in the world.

Huawei had secured cutting-edge communication ICs by outsourcing manufacturing to TSMC, but the Trump administration severed this relationship by tightening sanctions. In other words, it is a blockade against the miniaturization of IC chips. Huawei was then forced to change its outsourcing partner to China’s Semiconductor Manufacturing International Corporation (SMIC), causing a setback in IC technology.

The third phase was initiated by the Biden administration in 2022. This can be broadly divided into the following three points: (1) the “CHIPS and Science Act,” which encourages the construction of semiconductor fabs in the United States, was passed (August); (2) a comprehensive ban was imposed on exports to China of products related to the development and production of AI applications and ICs at 16/14nm process or below (October); and (3) flash memory manufacturer Yangtze Memory Technologies Corporation (YMTC) and AI IC fabless manufacturer Cambricon Technologies Corporation (Cambricon) were added to the EL (December).

The key is the comprehensive regulation in (2). The Trump administration added SMIC to the EL in December 2020, cutting off the export pathway for extreme ultraviolet (EUV) exposure equipment, which is essential for IC manufacturing at 10nm processes or below. EUV equipment is a very difficult technology, and only one company in the world, ASML of the Netherlands, supplies it.

(2) shows that the Biden Administration has been careful to extend export restrictions to DUV (deep ultraviolet) exposure equipment, which is a generation older than EUV equipment. (1) prohibits foreign companies that receive US government subsidies, such as TSMC, from improving the technological level of factories in China, while (3) imposes sanctions on individual companies that make memory and logic ICs for AI.

Taking (1), (2), and (3) of the third phase together, it is clear that the US government intends to curb China’s development and production of advanced IC chips for use in AI and other fields. Japan, which is strong in semiconductor materials and manufacturing equipment, introduced new export controls in July 2023, and the Netherlands did the same in September of that year, reinforcing the containment of China.

The Biden administration repeatedly announced semiconductor restrictions on China through the end of its term in January 2025. This move was a gradual expansion of (2) and (3) to prevent China from exporting through third countries and the rise of new Chinese companies.

In other words, the framework of the US government’s sanctions on China regarding semiconductors was largely established in the third phase, and the United States is now in a state of maintaining and reinforcing it. The outcome of US-China friction in “another Trump” era is expected to depend on how the second Trump administration evaluates this framework and how it changes it.

What has changed in China’s semiconductor industry?

So how have seven years of friction changed China’s semiconductor industry?

First, let’s look at the attitude of the Xi leadership. At the Central Economic Work Conference held in December 2024, the Communist Party decided on its economic management policy for 2025, and one of its priorities was to “through scientific and technological innovation, promote the application of AI.” Although there was no direct mention of semiconductors, the emphasis on semiconductors has not changed.

In early 2025, news broke that the third phase of the ICF (with a capital of 344 billion yuan), established in May 2024, had created two new funds to serve as an implementation force. The Communist Party and the government continue to inject direct funding.

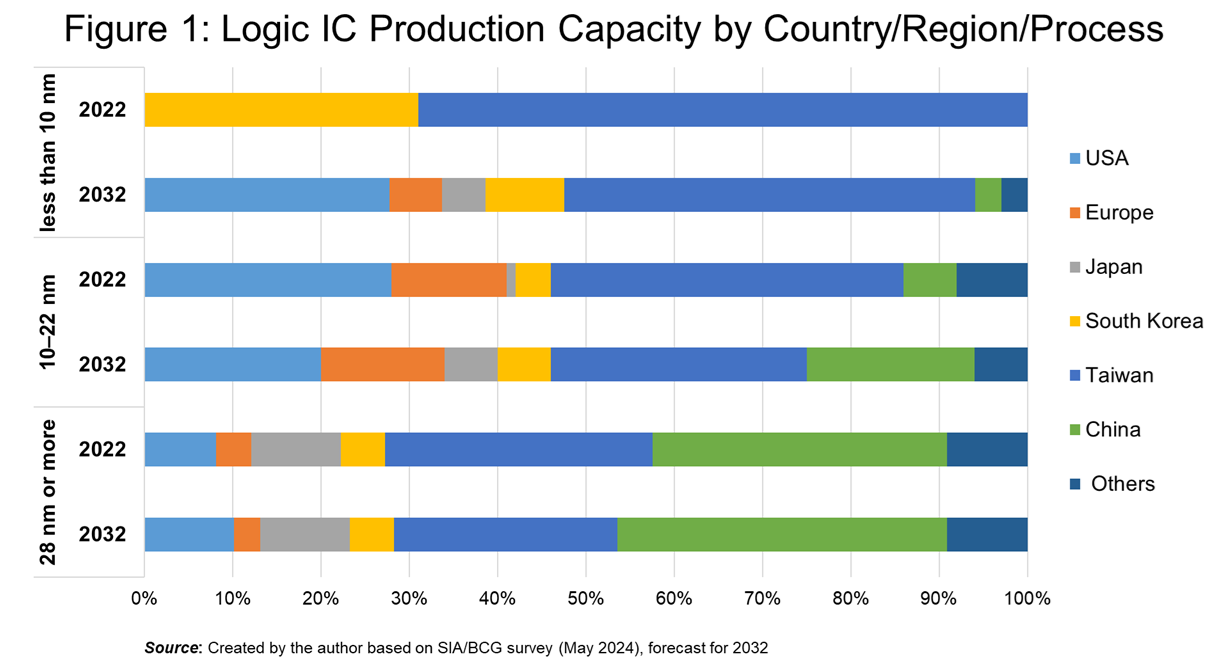

Next, let’s examine the changes in the semiconductor industry itself. In May 2024, the Semiconductor Industry Association (SIA) and the Boston Consulting Group (BCG) published a study that organized global semiconductor manufacturing capacity by country/region and process (Figure 1).

The series of US sanctions was aimed at preventing China from independently developing and producing cutting-edge logic ICs for communications and AI. In Figure 1, “less than 10 nm” represents the cutting edge. In 2022, the market share is split between Taiwan (69%), where TSMC is located, and South Korea (31%), where Samsung Electronics is located. This means that there were no manufacturers of advanced logic ICs in China at that time. It is possible that the US sanctions that had been in place for four years had some effect.

On the other hand, China has secured a certain production share of mature process logic ICs of “10–22 nm” and “28 nm or more.” These are mainly used in automobiles, home appliances and industrial equipment. By 2032, China’s share is expected to increase further, making it a production area on a par with Taiwan.

The simple total of the ICF up to the third phase is 686.7 billion yuan (about 93.88 billion dollars). This means that investment has been driven by a top-down approach typical of the Communist Party system. However, due to the anti-China containment that was completed in the third phase, Chinese manufacturers are unable to import cutting-edge semiconductor manufacturing equipment such as EUV equipment. As a result, a large amount of direct government funding has flowed into manufacturing equipment for mature processes, leading to a massive increase in production.

How well is self-sufficiency being achieved? In August 2023, Canadian research firm TechInsights released a forecast that China’s IC self-sufficiency rate would be 23.2% in the same year. This is far from the “80% by 2030” target set by “Made in China 2025.”

However, this is a significant improvement from the self-sufficiency rate (15.9%) calculated by the research company in 2015. In the first place, the basis for the self-sufficiency rate indicated by “Made in China 2025” is unclear. There is no doubt that the huge increase in production during the maturation process has significantly increased self-sufficiency rates.

To sum up, under the US-China friction, China’s semiconductor industry has spent the past seven years (1) failing to acquire the development and production capacity for advanced logic ICs, (2) significantly increasing the production capacity for mature processes, and (3) increasing the self-sufficiency rate, but not reaching the target.

The “miniaturization = competitiveness” structure is crumbling

By blocking miniaturization, the US government has succeeded in preventing China from developing and producing cutting-edge ICs for communications and AI. Importantly, there are signs that the “miniaturization = competitiveness” formula is beginning to break down in China’s semiconductor industry.

In December 2024, the online version of China Central Television (CCTV) published an article with the headline “While the United States is tightening its chip sanctions, China’s semiconductor exports have surpassed one trillion yuan.” It praised China’s semiconductor industry for battling to increase exports despite suffering from US sanctions.

Considering the global semiconductor market conditions and the large increase in mature semiconductor production in 2024, it is not surprising that China’s semiconductor exports will exceed 1 trillion yuan. However, this CCTV article raises two perspectives that undermine the idea that “miniaturization = competitiveness.”

One perspective is that AI performance is not determined by the IC process alone. This article points out that performance is “comprehensively influenced by many factors, including chip architecture (design structure), interconnect bandwidth (with memory), and optimization of algorithms (computational procedures).”

In early January 2025, the author had an opportunity to visit the Beijing headquarters of iFlytek, China’s leading AI company. The company is headquartered in Hefei, Anhui Province, but it also has a base in Beijing that serves as a development center and showroom.

The company was added to the EL in 2019, which means it can no longer import ICs such as the A100 made by Nvidia, the US leader in AI. Currently, it provides AI services for education and other purposes using the “Ascend 910B” IC designed by Huawei and manufactured by SMIC.

An iFlytek executive complained, “It would be easier if we could use Nvidia’s,” but explained, “There is no way to avoid the chip’s inferior computing power. We’ve developed an algorithm.” Initially, the performance was only 30% of the A100’s, but it is now back to almost the same level.

The fact that this Chinese startup, founded a year and a half ago, was the starting point of the “DeepSeek shock” in late January 2025 is proof that AI performance does not depend solely on ICs. Regardless of the company’s future prospects, it is likely that similar AI companies will continue to emerge in China in the future.

Another perspective is the importance of ICs that use mature processes. The CCTV article mentioned above points out that “in real management, those who have mastered mature semiconductor technology and markets can achieve healthy and sustainable growth.”

In November 2024, Switzerland’s STMicroelectronics announced that it would begin outsourcing the production of 40nm process logic ICs to China’s Hua Hong Semiconductor. The application is automotive. Safety is a top priority for automotive ICs, and mature processes with stable operation are widely used.

In China, the world’s largest automobile market, the proportion of new energy vehicles such as electric vehicles (EVs) in new car sales exceeded 40% in 2024. It is natural that the amount of ICs installed in new energy vehicles will increase. STMicroelectronics, a global leader in automotive applications, has production capacity in China and is poised to deeply penetrate the Chinese market.

If they have production bases in China, they don’t need to be overly excited about the “Trump tariffs.” According to Chinese media, STMicroelectronics’ competitors, Germany’s Infineon Technologies and the Netherlands’ NXP Semiconductors, are also pursuing similar plans. This will allow China to have the big European companies on its side.

How will they deal with the second Trump administration?

China’s semiconductor industry is gaining competitiveness through AI and the maturation process to circumvent the US government’s blockade on miniaturization. How will the second Trump administration deal with this? In November 2024, the Chinese research firm ICwise published five expected impacts of Trump’s return to power (Figure 2).

If the second administration accepts (4), it will impose additional sanctions on China. If the United States judges that the blockade against miniaturization is insufficient, it will strengthen the framework for the third phase in (2). If it proceeds with (1), there is a risk that the efforts of STMicroelectronics and others will be in vain, and a backlash from the European side can be expected.

In (3), they hope that relations between the US and Japan and Europe will deteriorate due to Trump’s tariffs and other factors, and that the anti-China containment network built by the Biden administration will loosen. In (5), they are wary that the return of semiconductor production to the US under the CHIPS and Science Act will fail and that the second administration will take unexpectedly strong measures to protect its high-tech hegemony.

As discussed in this article, semiconductors are a complex industry that is intertwined with technological advances and the international division of labor. Even taking into account Trump’s personality, predictions are difficult. But because Japan is an important part of it, the industry and policymakers must continue to exercise their minds.

Figure 2: Impact of Trump’s return to the presidency on Chinese semiconductors

| (1) Biden sanctions advanced technology, while Trump indiscriminately affects mature technology. |

| (2) Focus on advanced technologies and processes, and increase sanctions at any time. |

| (3) The future variables mainly depend on the cooperation of US allies. |

| (4) The previous US sanctions policy did not achieve the expected results. |

| (5) The decline of the US semiconductor industry is irreversible. Pay attention to the “final efforts” of the United States. |

Source: Created by the author based on an analysis report “The impact of Trump’s inauguration on Chinese semiconductors (特朗普上台对中国半导体的影响)” published by ICwise (芯谋咨询) in November 2024. https://mp.weixin.qq.com/s/JZjMS0Eg6eGCaLi857Ii9A (in Chinese)

Translated from “‘Bisaika-fuji’ Kawasu Chugoku no Handotai Sangyo (China’s Semiconductor Industry Avoids ‘Blockade Against Miniaturization’),” Voice, April 2025, pp. 86–93. (Courtesy of PHP Institute) [April 2025]

YAMADA Shuhei

Specially Appointed Professor, J. F. Oberlin University

Born in 1968. Joined Nihon Keizai Shimbun, Inc. (now Nikkei Inc.) in 1991. Graduated from the School of Political Science and Economics at Waseda University, and completed an EMBA in Foreign Companies at Peking University. He was stationed in Greater China for nine years, including serving as Taipei Bureau Chief and Chief of the China Headquarters. In Japan, he has a long history of reporting on manufacturing industries such as electronics and machinery. After working as Economist, Japan Center for Economic Research, he took up his current position in 2023. His co-authored books include Chugoku Fakuta: Ajia Domino no Seiji-keizai Bunseki (The China factor: A political and economic analysis of the Asian domino) (Nikkei Publishing), Shin Chugoku Sangyoron ― Sono Seisaku to Kyosoryoku (New China industrial theory: Its policies and corporate competitiveness) (Bunshindo).

Born in 1968. Joined Nihon Keizai Shimbun, Inc. (now Nikkei Inc.) in 1991. Graduated from the School of Political Science and Economics at Waseda University, and completed an EMBA in Foreign Companies at Peking University. He was stationed in Greater China for nine years, including serving as Taipei Bureau Chief and Chief of the China Headquarters. In Japan, he has a long history of reporting on manufacturing industries such as electronics and machinery. After working as Economist, Japan Center for Economic Research, he took up his current position in 2023. His co-authored books include Chugoku Fakuta: Ajia Domino no Seiji-keizai Bunseki (The China factor: A political and economic analysis of the Asian domino) (Nikkei Publishing), Shin Chugoku Sangyoron ― Sono Seisaku to Kyosoryoku (New China industrial theory: Its policies and corporate competitiveness) (Bunshindo).

Keywords

- Yamada Shuhei

- J. F. Oberlin University

- Japan Center for Economic Research

- China

- semiconductors

- ICs

- United States

- sanctions

- blockade against miniaturization

- Xi Jinping

- Trump

- national security

- China Integrated Circuit Industry Investment Fund

- ICF

- ICT equipment

- weapons

- Entity List

- Huawei

- TSMC

- YMTC

- Cambricon

- extreme ultraviolet

- EUV

- IC self-sufficiency

- miniaturization

- AI

- Nvidia

- iFlytek

- STMicroelectronics

- Hua Hong Semiconductor

- Trump tariffs

Related posts:

The Way to Revitalize Japan’s Economy: The Government Should Not Intervene in Prices and Business Activities

The Way to Revitalize Japan’s Economy: The Government Should Not Intervene in Prices and Business Activities

Where Is Rapidus Heading? Questions Raised about “Semiconductor Support” through Examination of Taiwan’s TSMC

Where Is Rapidus Heading? Questions Raised about “Semiconductor Support” through Examination of Taiwan’s TSMC

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

JAPAN ACQUIRES A STRUCTURAL TRADE DEFICIT AND LOOKS SET TO HAVE A CURRENT ACCOUNT DEFICIT IN 2015

STRIVING TO BE NUMBER ONE IN BATTERIES

WHAT GIVES KOREAN COMPANIES THEIR EDGE?

STRIVING TO BE NUMBER ONE IN BATTERIES

WHAT GIVES KOREAN COMPANIES THEIR EDGE?